find your solution.

search for solutions by category, industries, insights, and people.

find your solution.

search for solutions by category, industries, insights, and people.

search for solutions by category, industries, insights, and people.

search for solutions by category, industries, insights, and people.

The One Big Beautiful Bill Act (OBBBA) is one of the most sweeping and permanent updates to the U.S. tax code in recent history. While it offers long-awaited clarity on provisions from the Tax Cuts and Jobs Act (TCJA), it also introduces new rules, thresholds, and limitations that will significantly impact how high-net-worth individuals plan, give, and invest.

At Elliott Davis, we’ve been closely tracking the implications of this legislation. Below, we highlight consequential changes and what they mean for your financial strategy. For a more extensive analysis of the bill’s tax provisions, we encourage you to read our related insight or watch our recent webinar.

The OBBBA introduces a range of tax provisions with significant implications for individuals and business planning. Below are the key areas high-net-worth individuals should watch:

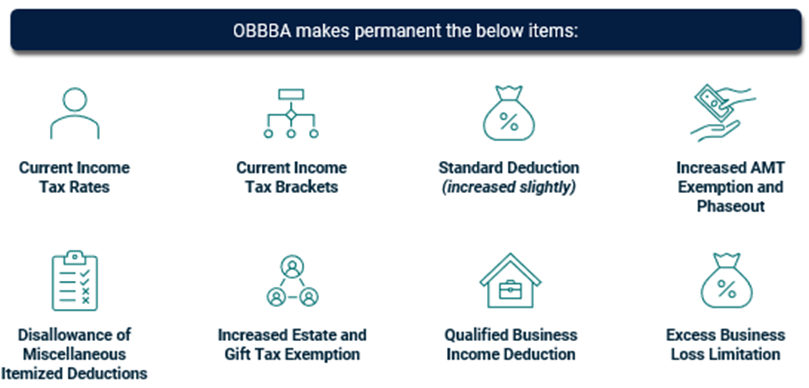

The OBBBA solidifies several cornerstone provisions of the TCJA that were scheduled to expire after 2025, including:

Keep in mind that “permanent” simply means that the provisions have no expiration date. It’s still possible that lawmakers could make changes to them in the future.

Before the bill, the top rate on passthrough business income was set to increase from 30% to 40% in 2026. By retaining the current top rate of 37% and the 20% qualified business income deduction, the bill maintains an effective top rate of roughly 30% on passthrough business income, preventing the significant tax rate increase that was anticipated for 2026.

Additionally, the reinstatement of 100% bonus depreciation, the ability to expense research and development (R&D) costs, and the adjustment to the business interest deduction limit may offer significant tax benefits and planning opportunities for business owners. It’s also important to understand how these changes may impact other tax attributes to help preserve additional benefits and optimize tax outcomes over time.

For 2025, the gift and estate tax exemption (the amount that can be transferred tax free during life or at death) is just under $14 million per person and was scheduled to be reduced to around $7 million per person in 2026. The bill increases the exemption to $15 million per person in 2026, establishes this amount the permanent base going forward, and indexes it for inflation in future years.

By increasing the exemption and making it permanent, the bill removes the urgency for certain taxpayers to make large gifts before year-end and offers additional exemption that wealthier taxpayers can use strategically. However, all taxpayers can benefit from continued planning. High-net-worth individuals should explore ways to shift future growth outside their taxable estate, while others may use the increased exemption to achieve a possible basis step-up to reduce gain or income taxes on appreciated assets. Everyone should review their current estate plan to confirm it still accomplishes their objectives and maximizes available tax savings.

Starting in 2026, two new limitations apply to the deduction for charitable gifts:

Since these changes are effective in 2026, it may be beneficial to accelerate charitable donations in 2025 for higher income taxpayers. For those who don’t itemize and are taking IRA distributions, qualified charitable distributions from their IRA remain a valuable way to generate tax savings.

However, these changes may reduce the effectiveness of traditional giving strategies, making it important to reassess timing and vehicles used for charitable contributions.

The State and Local Tax (SALT) deduction cap increases from $10,000 to $40,000 from 2025 through 2029, with a 1% annual increase. However, it remains subject to phaseouts based on modified adjusted gross income (MAGI), starting at $500,000. For taxpayers with MAGI over $600,000, the cap reverts to $10,000. This phaseout results in an effective federal rate of 45.5% on the next $100,000 of income above the $500,000 threshold. Taxpayers near or above this level may benefit from steps to reduce or manage their MAGI to avoid triggering the phaseout.

Many taxpayers will continue to benefit from electing to have passthrough entities pay state tax on business income at the entity level, commonly referred to as the pass-through entity (PTE) tax election, which can help bypass the individual SALT cap.

For moderate-income taxpayers, the timing of SALT payments and other itemized deductions, such as charitable donations, remains important. “Bunching” these deductions into a single tax year may help maximize their tax benefit.

Under pre-OBBBA law, up to $10 million of gain on the sale of QSBS held for at least five years was excludable for each taxpayer.

The OBBBA relaxes and expands the benefit of owning QSBS. Taxpayers are no longer required to own the stock for at least five years before receiving any gain exclusion benefit. Instead, taxpayers can exclude up to 50% of the gain for stock held for at least three years and up to 75% of the gain for stock held at least four years. Additionally, the gain exclusion amount is increased from $10 million per taxpayer to $15 million per taxpayer.

Since QSBS only applies to C corporation stock that meets certain criteria, properly structuring the ownership of a business that you intend to sell in the near future may generate significant tax savings.

While the permanence of the TCJA provisions offers stability, new deduction floors and benefit caps may diminish the effectiveness of some traditional strategies. At Elliott Davis, we help clients:

We’ve highlighted the most impactful changes for high-net-worth taxpayers, but the OBBBA includes several additional provisions worth noting. Starting in 2026, high earners in the 37% tax bracket will face new limits on itemized deductions. A cap on gambling loss deductions also takes effect next year. In addition, sole proprietors and pass-through businesses owners should be aware of new provisions that may directly affect their planning.

Given these tax law changes, it may be time to re-evaluate your financial strategy. Contact us today to discuss how the new tax code impacts your goals.

The information provided in this communication is of a general nature and should not be considered professional advice. You should not act upon the information provided without obtaining specific professional advice. The information above is subject to change.