find your solution.

search for solutions by category, industries, insights, and people.

find your solution.

search for solutions by category, industries, insights, and people.

search for solutions by category, industries, insights, and people.

search for solutions by category, industries, insights, and people.

Signed into law on July 4, 2025, the One Big Beautiful Bill Act (OBBBA) introduces several international tax changes that could affect manufacturers and distributors (M&D). While the overall impact may not be material for every company, understanding the nuances can help to identify planning opportunities and prepare for downstream effects.

Although the OBBBA’s international tax provisions may not significantly affect every M&D company’s income tax position, the changes are meaningful enough to warrant a fresh look at your global tax strategy. Each company’s situation is unique, and the new rules should be evaluated against your specific business profile. In many cases, the overall impact may be modest, but not universally so.

Introduced as part of the 2017 Tax Cuts and Jobs Act (TCJA), Global Intangible Low-Taxed Income (GILTI) refers to a category of foreign income subject to U.S. tax, even if that income hasn’t been sent back to the U.S. shareholder. This rule applies to foreign companies that are owned or controlled by U.S. persons. It works alongside other rules that also deal with foreign income to discourage companies from holding intangible assets in low-tax jurisdictions and preserve the U.S. tax base.

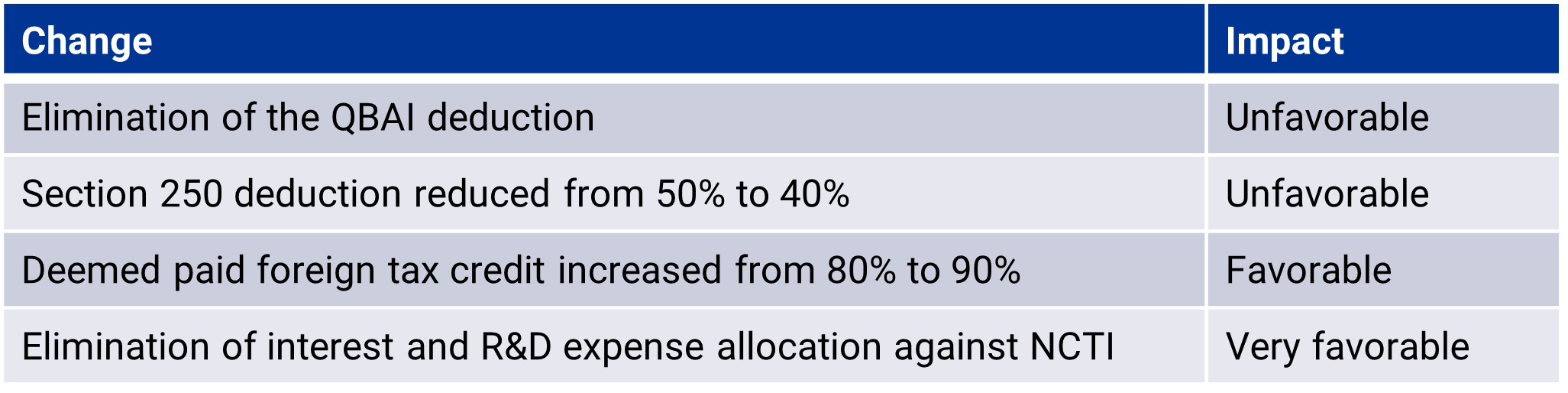

Before calculating the taxable amount, companies could subtract 10% of the average value of their tangible assets (like buildings or equipment) used in the foreign business through the Qualified Business Asset Investment (QBAI) deduction. After subtracting QBAI, companies could then deduct 50% of the remaining income under Section 250 (subject to a taxable income limitation), cutting the taxable amount in half. The U.S. corporate tax rate was (and remains) 21%, but because only half the income was taxed (thanks to the Section 250 deduction), the effective tax rate became 10.5%. Companies could use up to 80% of the foreign taxes they paid to reduce their U.S. tax bill further.

The OBBBA modifies several key aspects of what was previously known as the GILTI framework. Under the new law, GILTI has been officially renamed Net CFC Tested Income (NCTI). While this is the formal designation, it’s expected that many tax professionals will continue using both names interchangeably for some time.

The following table summarizes the changes and their potential impact on M&D companies:

Net effect: The pre-credit effective tax rate on NCTI rises from 10.5% to 12.6%. However, many international M&D companies may still benefit from the unchanged high-tax exception and enhanced foreign tax credits due to the elimination of the expense allocation. These adjustments could significantly reduce NCTI-related tax liability despite the rate increase.

At Elliott Davis, we recommend modeling your company’s worldwide tax rate under the new rules to pinpoint areas of exposure. Identifying these areas early can reveal structural or operational opportunities to reduce your tax burden.

If your NCTI or overall effective tax rate increases due to the unfavorable QBAI adjustment, a projected Foreign Derived Deduction Eligible Income (FDDEI) benefit may suggest that manufacturing assets could be more tax-efficiently deployed in the U.S., especially given the favorable treatment of domestic depreciable assets.

FDDEI, previously known as Foreign-Derived Intangible Income (FDII), was introduced under the TCJA to provide a tax deduction for companies that export goods and services to foreign jurisdictions. The OBBBA officially renamed FDII to FDDEI, reflecting a broader base that now includes returns from tangible assets, not just intangible ones. Under the original TCJA framework, the effective tax rate on qualifying FDII income was 13.125%, and under the OBBBA, this rate increases to 14%. Despite the rate change, FDDEI remains a valuable planning tool, and companies should consider claiming the deduction going forward or amending prior returns to claim the benefit.

For companies with significant R&D expenses offshore, the disparity between immediate expensing of domestic R&D and 15-year amortization of foreign R&D may justify a structural change. This may improve cash flow and better align your operations with the updated tax incentives introduced under the OBBBA, particularly for companies with substantial investments in innovation.

If restructuring is impractical, a “check-the-box” election for certain controlled foreign corporations may offer a simpler path. By filing Form 8832, a foreign corporation can be treated as disregarded for U.S. tax purposes.

Strategic advantages include:

This added flexibility can help companies optimize their structure and reduce long-term tax liability.

While the NCTI rate increase is real, the economic impact may be small. Before making structural changes, assess whether the changes are material enough to justify action. With QBAI removed from the FDDEI calculation, the deduction may now be more favorable for some taxpayers. Reassessing the net impact of FDDEI could reveal new opportunities to optimize your global tax footprint.

Since the law was enacted on July 4, 2025, calendar-year companies must reflect the changes in their Q3 tax provision. We recommend:

Taking early action can help avoid last-minute year-end provision adjustments.

The OBBBA introduces wide-ranging changes that are complex to interpret, and their full impact may take time to understand. From bonus depreciation and inventory sourcing to NCTI and FDDEI, the new rules require manufacturers to revisit their tax positions, entity structures, and financial models.

Elliott Davis is here to help you work through these changes by:

Now may be the time to re-evaluate your financial strategy. Contact us today to get started.

The information provided in this communication is of a general nature and should not be considered professional advice. You should not act upon the information provided without obtaining specific professional advice. The information above is subject to change.