find your solution.

search for solutions by category, industries, insights, and people.

find your solution.

search for solutions by category, industries, insights, and people.

search for solutions by category, industries, insights, and people.

search for solutions by category, industries, insights, and people.

After months of preparation, your real estate firm has the right people, the right systems, and the right capital in hand to close your first major property deal.

The path ahead is exciting, but decisions made during this next phase, particularly around purchase price allocation (PPA), can significantly affect your tax burden, cash flow, and future profits at sale. Too often, this step is rushed or overlooked entirely. But it’s one of the most strategic financial levers in the real estate capital cycle.

Let’s break it down.

When you acquire a property or a business that owns property, you must allocate the total purchase price across various asset categories, such as land, building, equipment, intangible assets, leases, and goodwill. This allocation becomes the foundation of your tax strategy, affecting depreciation schedules, expense timing, and eventual gain or loss recognition at sale.

The right strategy can accelerate depreciation, increase near-term tax deductions, and put you in a stronger financial position down the road.

In the real estate capital cycle, PPA takes place around closing, once the deal is finalized and the finance team is preparing to record the transaction. It’s a critical junction to pause and assess the following strategic questions:

A well-structured PPA can support audit readiness, tax efficiency, and valuation credibility.

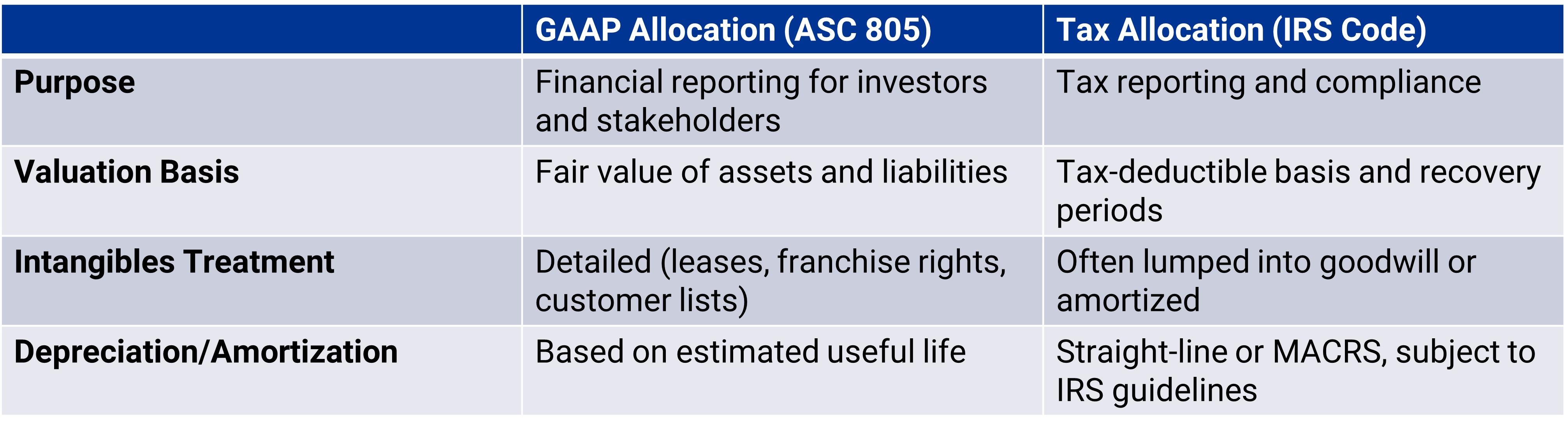

Here’s a breakdown of the differences between Generally Accepted Accounting Principles (GAAP) and IRS requirements:

Modified Accelerated Cost Recovery System (MACRS) is a depreciation system used by the IRS to recover the cost of tangible property over time for tax purposes.

When you allocate the purchase price of a hotel across asset classes like building, furniture, equipment, and land improvements, the IRS lets you depreciate many of those assets using MACRS schedules, which determine:

When you buy real estate, the transaction could be treated in two different ways under GAAP.

Business combination examples include:

If your deal is classified as a business combination under ASC 805:

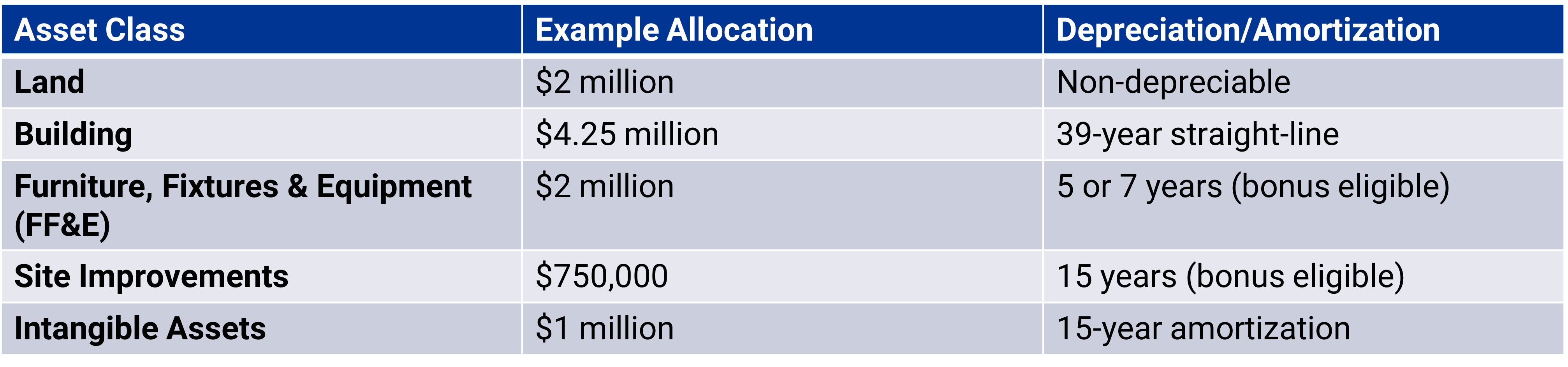

Consider a real estate firm purchasing a well-established, independently operated boutique hotel for $10 million. The property has stable operations, a consistent guest base, and long-term staff contracts. A common allocation might be:

This allocation strategy can improve tax benefits through accelerated depreciation and amortization, improving cash flow in the early years of ownership.

How you structure your PPA impacts everything from tax savings to your long-term exit strategy. The right mix can improve cash flow early in the hold period while the wrong one can trigger unfavorable tax consequences later.

Assets like furniture, fixtures, and landscaping often qualify for accelerated or bonus depreciation, delivering larger upfront deductions than the building itself. Cost segregation studies can help identify and support these faster-depreciating components.

Allocating to goodwill, franchise rights, or leases in place can offer amortization benefits, but over allocating to short-life assets like FF&E may lead to higher depreciation recapture taxes if you sell early. Know your holding period and align accordingly:

Institutional buyers or real estate investment trusts (REITs) may prefer different allocation profiles. Also, be aware that personal property (like FF&E) may be subject to annual taxes depending on your state, which can wipe out the benefits of faster depreciation.

Avoid relying exclusively on the bank’s appraisal when determining asset allocation. Include intangibles, factor in local tax rules, and revisit your allocation strategy as tax laws change. A tax advisor can help you strike the right balance between upfront tax savings and long-term return on investment (ROI).

At Elliott Davis, we work with growing real estate firms that are preparing for an acquisition or scaling into new markets. Our real estate team can:

Contact us today to get started.

The information provided in this communication is of a general nature and should not be considered professional advice. You should not act upon the information provided without obtaining specific professional advice. The information above is subject to change.

.avif)