find your solution.

search for solutions by category, industries, insights, and people.

find your solution.

search for solutions by category, industries, insights, and people.

search for solutions by category, industries, insights, and people.

search for solutions by category, industries, insights, and people.

In this edition of the quarterly communication, we have provided information about financial reporting and accounting issues – some of which are currently being evaluated by regulatory agencies and not resolved at this time. We have also compiled a list of items for consideration in your financial reporting and disclosures for the third quarter and a summary of recently issued accounting pronouncements (see Appendices for summary of recently issued accounting pronouncements and the related effective dates).

Click here to download the PDF.

The following selected Accounting Standards Updates (ASUs) were issued by the Financial Accounting Standards Board (FASB) during the third quarter. A complete list of all ASUs issued or effective in 2025 is included in Appendix A.

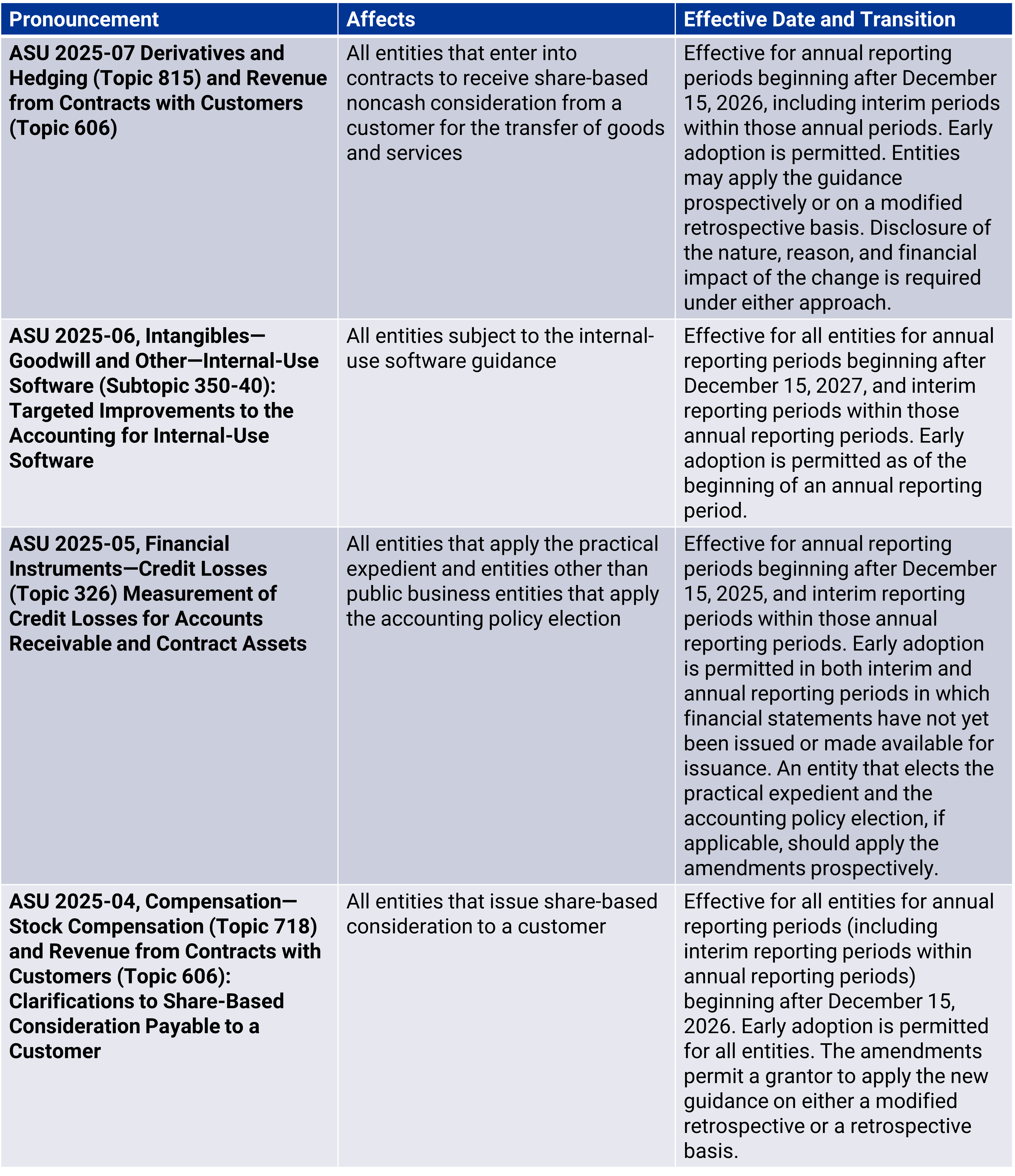

In September, the FASB issued ASU 2025-07, Derivatives and Hedging (Topic 815) and Revenue from Contracts with Customers (Topic 606), which addresses two key areas of stakeholder concern: (1) the application of derivative accounting to contracts with features tied to the operations or activities of one of the parties, and (2) the accounting treatment of share-based noncash consideration from customers in revenue contracts.

The first issue focuses on refining the scope of ASC 815 to exclude certain contracts that are not exchange-traded and whose underlying features are based on entity-specific activities. These contracts, including certain R&D and litigation funding arrangements, may now qualify for a scope exception. The ASU also clarifies the term “parties to the contract” in the context of the scope exception in ASC 815.

The second issue clarifies how entities should account for share-based payments received from customers under ASC 606. Specifically, such payments should be treated as noncash consideration and measured at fair value at contract inception. Changes in fair value are not recognized until the right to consideration becomes unconditional.

Effective Dates

ASU 2025-07 is effective for annual reporting periods beginning after December 15, 2026, including interim periods within those annual periods. Early adoption is permitted. Entities may apply the guidance prospectively or on a modified retrospective basis. Disclosure of the nature, reason, and financial impact of the change is required under either approach.

In July, the FASB issued ASU 2025-05, Financial Instruments—Credit Losses (Topic 326) Measurement of Credit Losses for Accounts Receivable and Contract Assets, that improves guidance on the measurement of credit losses for accounts receivable and contract assets. The Private Company Council (PCC) initiated this standard-setting activity in response to feedback from private company stakeholders. Although this standard is unlikely to directly impact financial institutions, it could influence the financial statements of their borrowers.

Note: Separately, in April, the FASB voted to eliminate the CECL “double count” issue and expects to issue a final standard later this year. This decision reflects ongoing efforts to refine CECL implementation and reduce unintended complexity in credit loss measurement.

The new guidance, which is optional, addresses challenges faced when applying Accounting Standards Codification (ASC) 326, Financial Instruments—Credit Losses, to current accounts receivable and current contract assets arising from transactions accounted for under ASC 606, Revenue from Contracts with Customers. These challenges included the cost and complexity of developing a reasonable and supportable forecast when estimating expected credit losses and the significant effort to estimate and record expected credit losses for current accounts receivable and current contract assets that were collected before the date that the financial statements were available to be issued.

To address this feedback, the amendments in this ASU provide (1) all entities with a practical expedient to assume that current conditions as of the balance sheet date do not change for the remaining life of the assets and (2) entities other than public business entities with an accounting policy election to consider collection activity after the balance sheet date when estimating expected credit losses for current accounts receivable and current contract assets arising from transactions accounted for under ASC 606.

Effective Dates

The amendments will be effective for annual reporting periods beginning after December 15, 2025, and interim reporting periods within those annual reporting periods. Early adoption is permitted in both interim and annual reporting periods in which financial statements have not yet been issued or made available for issuance. An entity that elects the practical expedient and the accounting policy election, if applicable, should apply the amendments in this Update prospectively.

An entity other than a public business entity that elects the practical expedient and, if applicable, the accounting policy election after the effective date would not need to perform a preferability assessment in accordance with ASC 250, Accounting Changes and Error Corrections.

In September, the FASB issued ASU 2025-06, Intangibles—Goodwill and Other—Internal-Use Software (Subtopic 350-40): Targeted Improvements to the Accounting for Internal-Use Software, that updates the guidance on accounting for internal-use software costs. The amendments apply to all entities subject to guidance in FASB Accounting Standards Codification (ASC) Subtopic 350-40, Intangibles—Goodwill and Other—Internal-Use Software.

Under current U.S. generally accepted accounting principles (U.S. GAAP), entities are required to capitalize development costs incurred for internal-use software depending on the nature of the costs and the project stage during which they occur. Stakeholders said that applying this guidance can be challenging because entities have trouble differentiating between the project stages, particularly in an iterative development environment (for example, agile).

The amendments in this ASU improve the operability of the guidance by removing all references to software development project stages so that the guidance is neutral to different software development methods, including methods that entities may use to develop software in the future. Therefore, the amendments require that an entity capitalize software costs when both:

In evaluating the probable-to-complete recognition threshold, an entity is required to consider whether there is significant uncertainty associated with the development activities of the software.

Effective Dates

The amendments are effective for all entities for annual reporting periods beginning after December 15, 2027, and interim reporting periods within those annual reporting periods. Early adoption is permitted as of the beginning of an annual reporting period.

At the September 2025 meeting of the Financial Stability Oversight Council, FDIC Acting Chairman Travis Hill issued a statement outlining reforms to streamline supervision, modernize capital standards, clarify digital asset policies, and improve resolution planning. Additional efforts include addressing debanking concerns, encouraging new bank formation, and rescinding outdated policies to support economic growth while maintaining financial stability.

On July 15, 2025, the FDIC published a notice of proposed rulemaking that would raise asset thresholds for certain regulatory requirements to better reflect inflation and reduce burdens on community banks.

Threshold Increases

Inflation Indexing

Future adjustments to the thresholds will be tied to Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W), with adjustments occurring every two years or sooner if inflation exceeds 8%.

Effective Dates

Comments on the proposal were due by September 26, 2025. Initial changes begin the first calendar quarter after final rule adoption. Future inflationary adjustments will occur every April 1 of the adjustment year.

On August 26, 2025, the FDIC released its most recent Quarterly Banking Profile covering the second quarter of 2025. The Quarterly Banking Profile is a quarterly publication that provides the earliest comprehensive summary of financial results for all FDIC-insured institutions. The report includes data from 4,421 commercial banks. Highlights from the Second Quarter 2025 Quarterly Banking Profile are included below:

On August 15, 2025, the OCC released its annual update to the Bank Accounting Advisory Series (BAAS). This publication contains responses to frequently asked questions from the banking industry and bank examiners on a variety of accounting topics and promotes consistent application of accounting standards and regulatory reporting among banks. In this edition of the BAAS, there with no substantive changes, but clarified existing guidance through revisions, removals, and renumbering.

On June 30, 2025, the OCC released its “Semiannual Risk Perspective” affirming the overall soundness of the federal banking system but flagging rising risks across credit, market, operational, and compliance areas.

Federal banking agencies reaffirmed that banks may offer crypto asset safekeeping if done safely and in compliance with existing laws. The joint statement does not create new regulations but outlines risk considerations around cryptographic key control, legal compliance, third-party oversight, and audit practices, without adding new supervisory expectations.

As part of his goal to “make IPOs great again,” Securities and Exchange Commission (SEC) Chair, Paul Atkins, in September, indicated that SEC staff is working on proposal for semiannual reporting by public companies. This comes as President Trump has urged the SEC to revise the reporting rules so that public companies would not need to report on a quarterly basis.

Atkins briefly addressed the concept of semiannual reporting during an open SEC meeting on September 17, which was held to vote on initial public offering (IPO) and mandatory arbitration clauses. He described these measures as among the first steps of his goal to reinvigorate IPO activity. Atkins stated that the bigger project is intended to make becoming a public company more attractive by eliminating compliance requirements that do not provide meaningful investor protections, minimizing regulatory uncertainty, and reducing legal complexities in the SEC's rulebook.

This is not the first time that the SEC has studied the timing, nature, and content of financial reporting. During his first term, Trump asked the SEC to consider the six-month reporting system to replace the three-month quarterly and annual filing requirements that U.S. public companies have followed since 1970. Trump at the time made the request after a business executive told him that quarterly reporting is too burdensome. Some critics of the current system also argue that quarterly reporting promotes a short-term mindset among corporate executives who are driven to meet earnings expectations every three months.

At the time, SEC Chair, Jay Clayton, initiated a study first by issuing a preliminary rulemaking document asking for feedback, then following up with a roundtable. After that, he kept delaying issuing a proposal, and there was no further regulatory movement. Then Gary Gensler, President Biden’s appointee to lead the SEC, quietly dropped the rulemaking in 2021 shortly after he took office.

In comment letters, in response to the preliminary rulemaking, businesses stated a clear preference for less frequent reporting. Moreover, in the spring of 2018, eight business organizations, including the U.S. Chamber of Commerce, the Securities Industry and Financial Markets Association (SIFMA), and the National Venture Capital Association, recommended reducing the frequency of regulatory filings as one of several policy initiatives to help more companies go and stay public. Business groups often say the decline in the number of IPOs compared to the 1990s is partly a result of unnecessary regulation.

On September 17, 2025, the SEC voted 3-1 along party lines to reverse a long-standing but unwritten SEC policy in which the agency blocked IPOs of companies that wanted to ban shareholder class action lawsuits in their charters and bylaws. The SEC said it would allow companies seeking to go public to require that investors resolve claims of fraud or other false statements through arbitration rather than court litigation, handing a victory to companies and weakening investor rights. The SEC issued a policy statement, rather than a formal rule, meaning it is not subject to public notice and comment.

Caroline Crenshaw, the SEC’s lone remaining Democrat, lambasted the new policy, saying it would open the floodgates to mandatory arbitration, denying many shareholders their rights while allowing companies to keep their alleged misconduct in the shadows. If harmed investors cannot band together in a class action, thereby sharing their legal costs, many simply won’t sue at all, she added.

Corporate interest groups and Republicans have long complained about what they see as the frivolous filing of shareholder class action suits, saying companies should be able to protect themselves. During President Trump’s previous administration, the agency considered such a change but ultimately took no action.

Consumer advocates and plaintiffs' lawyers say court action helps hold companies to account, gives small investors the chance to recover damages they otherwise couldn't, and gives the public access to evidence and legal reasoning that helps build case law and inform public policy.

On August 27, 2025, the SEC issued a new Compliance and Disclosure Interpretation (C&DI) on the application of Rule12b-2. The interpretation addresses the smaller reporting company revenue test in determining filer status changes, clarifying how issuers should evaluate their status over time and how that affects future filer classifications.

On July 2, 2025, the SEC announced it had published updates to the Financial Reporting Manual (FRM). The updated FRM incorporates changes to Regulation S-X Acquisition Rules 3-05, 3-14, 8-04, and 8-06. Additional revisions were made to reflect the 2020 amendments to Rules 3-10 and 3-16 relating to financial disclosures for guaranteed securities.

Note that the current update does not include revisions related to other rulemakings.

In September 2025, the agency responsible for implementing climate disclosure regulations in California issued draft guidance to assist the companies that are required to publish their first reports by January 1, 2026. While the SEC paused legal defense of its climate rule in February 2025, essentially shelving it for the foreseeable future, a state that qualifies on its own as one of the world’s largest economies continues to move forward with climate-related legislation. The California Air Resources Board (CARB) released guidance for complying with the Climate Related Financial Risk Disclosure Program, which features a law (S.B. 261) requiring companies with at least $500 million in revenues to file climate risk reports every other year.

In March 2025, the AICPA and the California Society of CPAs asked CARB in a joint comment letter to consider clarifications when developing regulations that ensure CPAs can effectively support a practical and efficient climate disclosure framework. The draft guidance states that a reporting entity may use one of several frameworks to meet disclosure requirements:

CARB said at a public meeting last month that it is aiming to issue proposed regulations in October for S.B. 261 as well as S.B. 253, a law requiring companies with more than $1 billion in revenue to report greenhouse gas emissions annually. Following a 45-day public comment period, CARB will consider issuing the rules in early December.

The following selected FASB proposed ASUs, exposure drafts and projects were either newly introduced or updated as well as activities of the EITF and the PCC during the quarter ended September 30, 2025.

The Emerging Issues Task Force (EITF) met on September 9, 2025, and deliberated the following topic:

a. Pension benefits are communicated to employees in the form of a current account balance that is based on principal credits and interest credits based on an investable market return based on:

b. Participants have the option to elect lump-sum payments.

The EITF recommended that the proposed changes should be required for all entities. The EITF recommended not requiring additional disclosures beyond those currently required under generally accepted accounting principles. The EITF recommended that the proposed changes may be applied either prospectively or retrospectively, with early adoption permitted.

The FASB will discuss this issue at a public meeting to determine whether to add a project to the FASB’s technical agenda. The EITF’s recommendations do not constitute an amendment to GAAP.

The Private Company Council (PCC) met on June 26, and June 27, 2025. Below is a summary of topics discussed by PCC and FASB members at the meeting:

The following table contains significant implementation dates and deadlines for standards issued by the FASB and others.

The illustrative disclosures below are presented in plain English. Please review each disclosure for its applicability to your organization and the need for disclosure in your organization’s financial statements. For the items listed, the Company does not expect these amendments to have a material effect on its financial statements. Other accounting standards issued or proposed by the FASB or similar bodies are likewise not expected to have a material impact on the Company’s financial position, results of operations, or cash flows.

Applicable to insurance entities issuing long-duration contracts:

In August 2018, the FASB amended the Financial Services—Insurance Topic of the Accounting Standards Codification to make targeted improvements to the existing recognition, measurement, presentation, and disclosure requirements for long-duration contracts issued by an insurance entity.

Effective Dates

Applicable to insurance entities issuing long-duration contracts:

In November 2020, the FASB issued guidance to defer the effective dates for insurance entities which have not yet applied the long duration contracts guidance by one year.

Effective Dates

Applicable to all entities:

In June 2022, the FASB issued amendments to clarify the guidance on the fair value measurement of an equity security that is subject to a contractual sale restriction and require specific disclosures related to such an equity security. Early adoption is permitted.

Effective Dates

Applicable to insurance entities that have derecognized contracts before the effective date of ASU 2018-12:

In December 2022, the FASB issued amendments to reduce implementation costs and complexity associated with the adoption of ASU 2018-12 for contracts that have been derecognized in accordance with the amendments in this ASU before the effective date of ASU 2018-12.

Effective Dates

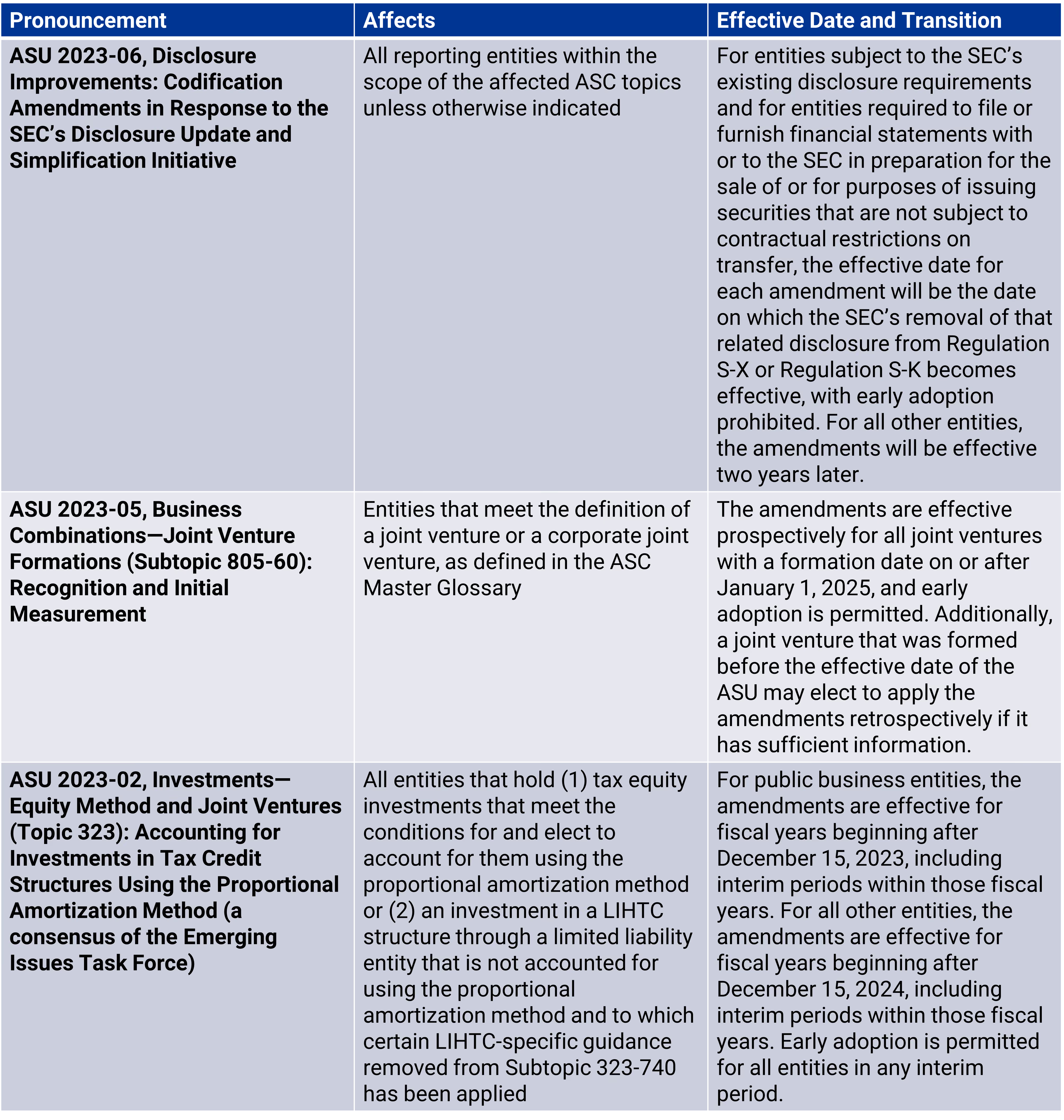

Applicable to all entities that hold (1) tax equity investments that meet the conditions for and elect to account for them using the proportional amortization method or (2) an investment in a LIHTC structure through a limited liability entity that is not accounted for using the proportional amortization method and to which certain LIHTC-specific guidance removed from Subtopic 323-740 has been applied:

In March 2023, the FASB issued amendments to allow reporting entities to consistently account for equity investments made primarily for the purpose of receiving income tax credits and other income tax benefits. Early adoption is permitted for all entities in any interim period.

Effective Dates

Applicable to Entities meeting the definition of a joint venture or a corporate joint venture, as defined in the ASC Master Glossary:

In August 2023, the FASB issued amendments to address the accounting for contributions made to a joint venture, upon formation, in a joint venture’s separate financial statements. Early adoption is permitted in any interim or annual period in which financial statements have not yet been issued (or made available for issuance), either prospectively or retrospectively.

Effective Dates

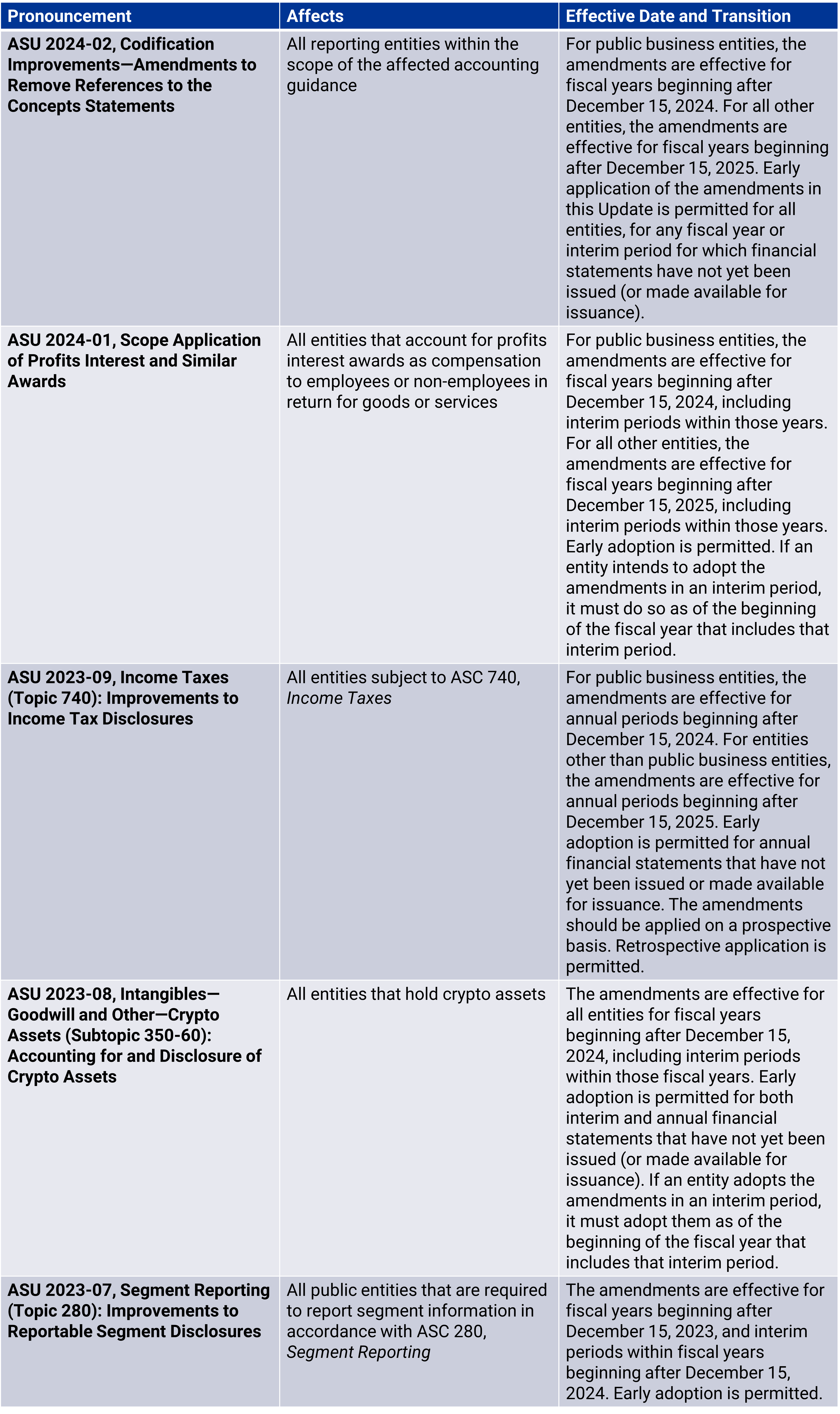

Applicable to all reporting entities within the scope of the affected ASC topics unless otherwise indicated:

In October 2023, the FASB issued amendments to incorporate certain U.S. Securities and Exchange Commission (SEC) disclosure requirements into the U.S. GAAP and align the requirements with the SEC’s regulations. Early adoption is prohibited.

Effective Dates

Applicable to all public entities that are required to report segment information in accordance with ASC 280, Segment Reporting:

In November 2023, the FASB amended the Segment Reporting topic in the Accounting Standards Codification to improve disclosures about a public entity’s reportable segments and provide more detailed information about a reportable segment’s expenses. Early adoption is permitted.

Effective Dates

Applicable to all entities that hold crypto assets:

In December 2023, the FASB amended the Intangibles topic in the Accounting Standards Codification to improve the accounting for and disclosure of certain crypto assets. Early adoption is permitted.

Effective Dates

Applicable to all entities subject to ASC 740, Income Taxes:

In December 2023, the FASB amended the Income Taxes topic in the Accounting Standards Codification to improve the transparency of income tax disclosures. Early adoption is permitted for annual financial statements that have not yet been issued or made available for issuance.

Effective Dates

Applicable to all entities that account for profits interest awards as compensation to employees or nonemployees in return for goods or services:

In March 2024, the FASB amended the Compensation—Stock Compensation topic in the Accounting Standards Codification to demonstrate how an entity should apply the guidance to determine whether profits interest and similar awards should be accounted for in accordance with that topic. Early adoption is permitted for both interim and annual financial statements that have not yet been issued or made available for issuance.

Effective Dates

The Company will apply the amendments:

Applicable to all entities within the scope of the affected accounting guidance:

In March 2024, the FASB issued amendments to the Codification that remove references to various FASB Concepts Statements. Early adoption is permitted for both interim and annual financial statements that have not yet been issued or made available for issuance.

Effective Dates

The Company will apply the amendments:

Applicable to all public business entities:

In November 2024, the FASB amended the Income Statement—Reporting Comprehensive Income topic in the Accounting Standards Codification to require public companies to disclose, in interim and annual reporting periods, additional information about certain expenses in the notes to financial statements. Early adoption is permitted.

Effective Dates

The Company will apply the amendments:

Applicable to all entities that settle convertible debt instruments for which the conversion privileges were changed to induce conversion:

In November 2024, the FASB amended the Debt topic in the Accounting Standards Codification to clarify requirements for determining whether certain settlements of convertible debt instruments should be accounted for as an induced conversion. Early adoption is permitted for all entities that have adopted the amendments in ASU 2020-06.

Effective Dates

The Company will apply the amendments:

Applicable to all public business entities:

In January 2025, the FASB amended the effective date of ASU 2024-03 to clarify that all public business entities are required to adopt the guidance in annual reporting periods beginning after December 15, 2026, and interim periods within annual reporting periods beginning after December 15, 2027.

Applicable to all public business entities:

In March 2025, the FASB amended an SEC paragraph in the Accounting Standards Codification pursuant to the issuance of SEC Staff Accounting Bulletin No. 122. The amendment was effective upon issuance.

Applicable to all entities that issue share-based consideration to a customer:

In May 2025, the FASB amended the Business Combinations and Consolidation topics in the Accounting Standards Codification to revise current guidance for determining the accounting acquirer for a transaction effected primarily by exchanging equity interests in which the legal acquiree is a VIE that meets the definition of a business. Early adoption is permitted as of the beginning of an interim or annual reporting period.

Effective Dates

Applicable to all entities engaging in acquisition transactions involving a VIE:

In May 2025, the FASB amended the Stock Compensation and Revenue from Contracts with Customers topics in the Accounting Standards Codification to clarify the requirements for share-based consideration payable to a customer that vests upon the customer purchasing a specified volume or monetary amount of goods and services from the entity. Early adoption is permitted.

Effective Dates

The Company will apply the amendments:

Applicable to all entities engaging in acquisition transactions involving a VIE:

In July 2025, the FASB amended the Financial Instruments—Credit Losses topic in the Accounting Standards Codification to introduce a practical expedient for all entities and an accounting policy election for entities other than public business entities related to applying the current expected credit loss model to current accounts receivable and current contract assets. Early adoption is permitted in both interim and annual reporting periods in which financial statements have not yet been issued or made available for issuance.

Effective Dates

Applicable to all entities subject to the internal-use software guidance:

In September 2025, the FASB amended the Internal-Use Software subtopic in the Accounting Standards Codification to update the guidance on accounting for internal-use software costs. Early adoption is permitted as of the beginning of an annual reporting period.

Effective Dates

The Company will apply the amendments:

Applicable to all entities entering contracts to receive share-based noncash consideration:

In September 2025, the FASB amended the Derivatives and Hedging and Revenue from Contracts with Customers topics in the Accounting Standards Codification to refine derivative scope and clarify the accounting treatment of share-based noncash consideration from customers in revenue contracts. Early adoption is permitted.

Effective Dates

Note: The disclosures in the previous appendix are not intended to be all inclusive. All pronouncements issued during the period should be evaluated to determine whether they are applicable to your Company. Through September 30, 2025, the FASB has issued the following Accounting Standard Updates during the year.

The information provided in this communication is of a general nature and should not be considered professional advice. You should not act upon the information provided without obtaining specific professional advice. The information above is subject to change.

%20(1).jpg)