find your solution.

search for solutions by category, industries, insights, and people.

search for solutions by category, industries, insights, and people.

search for solutions by category, industries, insights, and people.

The time value of money is a component of every economic damages analysis involving future losses, yet it remains an area in which courts offer little guidance. Opinions from the courts on acceptable methods for identifying and implementing an appropriate discount rate are often specific to the facts of individual cases and therefore are not universally applicable. The discount rate tends to star as a frequent point of contention in litigious matters, and attorneys with an understanding of the concepts and factors of discount rates have the upper hand in articulating to judges and juries why their expert’s calculation is correct.

The concept of the time value of money acknowledges that there is a difference in the value of money at any two points in time. In awarding economic damages, courts often award an exact amount to a plaintiff as of the date of judgment, which requires a measurement of the difference in the value of money at the judgment date and at each future point in time that losses are expected to be incurred. Through this analysis, the court and experts aim to make the plaintiff whole for any losses sustained due to the defendant’s alleged misconduct.

To measure the time value of money in an economic damages analysis, experts use discount rates and interest rates, which are based on the notion that a dollar invested today will grow to be worth more in the future. Discount rates reduce future dollar amounts to the present value of the future dollar amount, while interest rates grow present dollar amounts to the future value of the present dollar amount. These instruments reflect two important concepts: 1) there is value to the use of money for a period of time, also known as opportunity cost; and 2) the present value of a dollar amount is affected by the risk in achieving the projected future value of that dollar amount. The remainder of this article will focus on methods and applications of discount rates.

The formula for discounting a future dollar amount to its present value is quite simple:

Present Value = Future Value / (1 + Discount Rate)Number of Periods

When one applies this formula to an example with a $1,100 Future Value and 10% Discount Rate for a 1 Year period, the result is a Present Value of $1,000.

$1,000 = $1,100 / (1 + 10%)1

While present value calculations are simple in theory and in their most basic form, performing and, perhaps more importantly, supporting any assumptions made in such calculations in an economic damages analysis can become complex quickly.

By breaking down the components of the calculation, one quickly sees why discount rates have the potential for contention in litigious matters. The Future Value is calculated from and supported by, evidence in the record, such as tax returns and financial statements. The number of periods is likewise calculated from evidence in the record or authoritative guidance such as work-life tables and life tables. The Discount Rate, while calculated based on publicly available financial data, is subject to an expert’s discretion, and small changes to inputs and assumptions can yield wide-ranging Present Values.

An expert must ensure that a discount rate accounts for both the time value of money and the risk of achieving the projected future cash flow. Higher discount rates reflect greater risk in the realization of future cash flows. For example, cash flow in the form of salary to a long-tenured employee likely carries less risk than cash flow in the form of business income to a new business owner. Therefore, one would expect the discount rate applied to the projected salary cash flow to be lower than that of the projected business income cash flow.

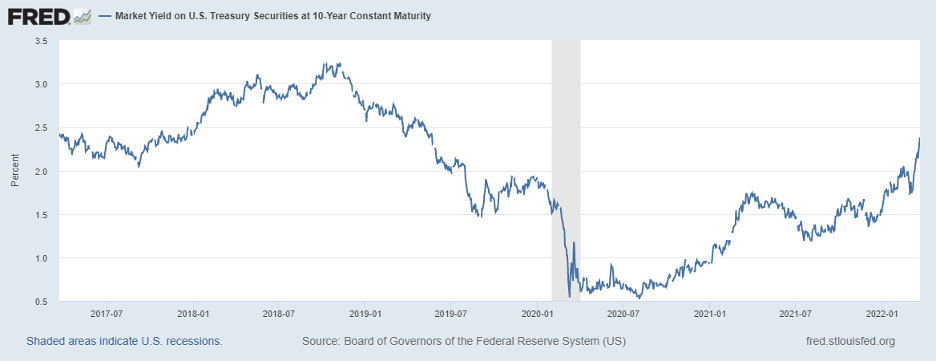

In some cases, like personal injury, wrongful death, and wrongful termination suits, courts have set precedent that a plaintiff is entitled to a risk-free stream of future income to replace lost wages. U.S. Treasury securities are often utilized as risk-free rates of return. Still, an expert is faced with the decision of which Treasury securities to select. An expert may select the spot rates of securities with maturities in each year of future cash flow. However, in rate environments where spot rates are not in line with historical averages and are not expected to continue in the future, a practitioner should be wary of using temporarily suppressed or inflated rates. One such recent rate environment was due to the COVID-19 pandemic, during which yields on Treasury securities were temporarily suppressed as shown below.

Of additional importance in the present value calculation is matching the number of periods with the timing of the cash flow. For example, cash flows occurring as a lump sum at the end of a year should be discounted over the entire period. In contrast, cash flows occurring evenly throughout the year, such as a flat salary, should be discounted for one-half of a period by utilizing a mid-period convention. A seemingly minor change like this can dramatically impact a present value calculation, and practitioners should be wary of calculations that do not properly match cash flow timing with the number of periods.

As a law practitioner, it’s helpful to be knowledgeable about issues like the time value of money in economic damages calculations. Think you might need the assistance of a skilled practitioner? Elliott Davis is ready with a team of professionals dedicated to issues like this. Contact us for more information.

REFERENCES

Tregillis, Christian, et al. “Discount Rates, Risk, and Uncertainty in Economic Damages Calculations.” AICPA (2020).

Jones & Laughlin Steel Corp. v. Pfeifer, 462 U.S. 523, 537 (1983)

The information provided in this communication is of a general nature and should not be considered professional advice. You should not act upon the information provided without obtaining specific professional advice. The information above is subject to change.